Price trends for organic vs conventional wheat show a persistent structural premium driven by supply rigidity, certification barriers, and steady consumer demand growth. Conventional wheat prices respond to global futures markets and export cycles, while organic wheat prices move independently within contract-based regional markets. This divergence has shaped agricultural profitability for more than a decade.

Over the past fifteen years, price trends for organic vs conventional wheat have consistently reflected a premium range of 50% to 120%. Understanding these price trends for organic vs conventional wheat is essential for farmers, investors, and agribusiness operators planning long-term production strategies.

Keyword Takeaway

- Price trends for organic vs conventional wheat show a consistent structural premium, with organic wheat trading 50% to 120% above conventional wheat over the past decade.

- Organic wheat prices are less correlated with global futures markets, while conventional wheat prices react quickly to export restrictions, weather shocks, and macroeconomic volatility.

- Lower supply elasticity in organic production supports premium stability, as certification requirements limit rapid acreage expansion.

- Per-acre profitability for organic wheat is often higher, despite lower yields, due to stronger market pricing.

- Long-term price trends for organic vs conventional wheat suggest continued divergence rather than convergence through 2035.

Table of Contents

- Structural Differences Behind Price Trends for Organic vs Conventional Wheat

- Historical Price Trends (2010–2026 Data Review)

- Organic vs Conventional Wheat Price Premium Analysis

- Yield, Cost, and Productivity Economics

- Profitability Modeling per Acre

- Volatility and Risk Assessment

- USDA-Style Forecast Model (2026–2035)

- Demand Growth and Consumer Behavior

- Strategic Implications for US Farmers and Investors

- What This Means for U.S. Investors

- FAQ

- Final Strategic Outlook

- Disclaimer

- Author

Structural Differences Behind Price Trends for Organic vs Conventional Wheat

The foundation of price trends for organic vs conventional wheat lies in market design. Conventional wheat trades on highly liquid futures exchanges where prices adjust instantly to export restrictions, drought conditions, fertilizer costs, and currency fluctuations. This global integration increases volatility.

Organic wheat follows a different pricing structure. It is sold primarily through negotiated regional contracts. Production requires a three-year transition period and strict certification compliance. These constraints limit rapid acreage expansion and create structural price stability.

Because of these fundamental differences, price trends for organic vs conventional wheat often diverge during periods of global disruption. Organic markets tend to move more gradually, while conventional wheat prices react sharply to macroeconomic shocks.

Historical Price Trends (2010–2026 Data Review)

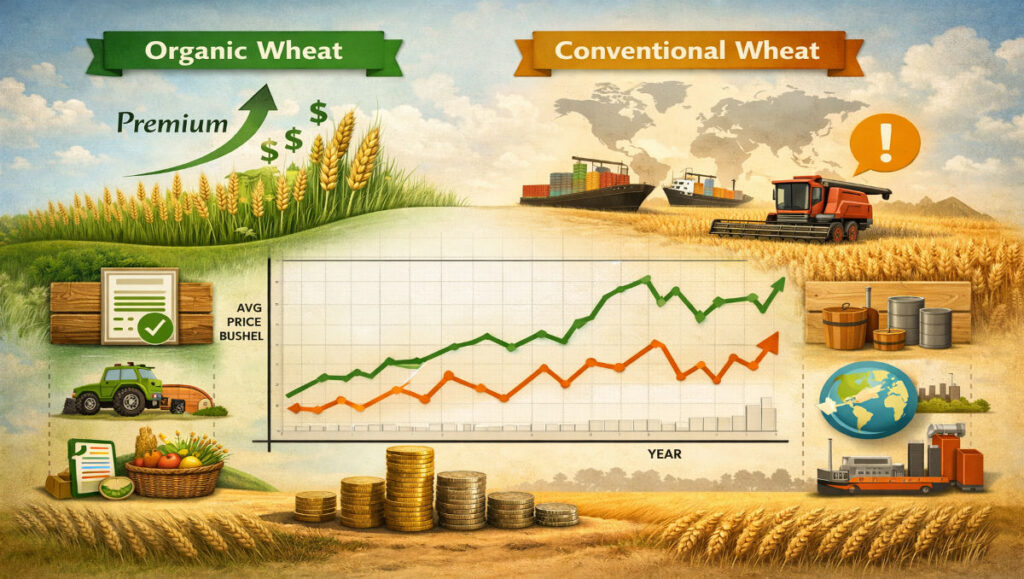

Between 2010 and 2019, conventional wheat prices averaged approximately $5.00 per bushel. During the same period, organic wheat prices averaged close to $10.50 per bushel. The premium remained consistent across multiple crop cycles.

In 2022, conventional wheat prices surged above $12.00 per bushel due to geopolitical supply disruptions. Organic wheat prices increased but did not experience the same amplitude of volatility. Instead, the premium adjusted moderately while preserving structural divergence.

For broader grain market context, review our detailed analysis on US Commodity Prices Today: Gold, Silver & Crude Oil Market Snapshot, which explains how macro volatility influences agricultural commodities across cycles.

From 2023 through 2026, conventional wheat stabilized between $6.00 and $7.00 per bushel. Organic wheat remained within $11.00 to $14.00 per bushel. These data points reinforce long-term price trends for organic vs conventional wheat that favor sustained premium positioning.

According to long-term data from the USDA Economic Research Service, historical wheat price series confirm the sustained premium pattern observed in organic markets compared to conventional production

Organic vs Conventional Wheat Price Premium Analysis

The premium embedded in price trends for organic vs conventional wheat typically averages near 70 percent under balanced supply conditions. During certified supply shortages, the premium can exceed 100 percent. In years of accelerated acreage expansion, the spread may compress toward 50 percent.

Unlike conventional wheat production, organic acreage cannot expand quickly because farmers must complete a multi-year transition. This supply rigidity supports the long-term stability of price trends for organic vs conventional wheat and reduces the likelihood of abrupt premium collapse.

Yield, Cost, and Productivity Economics

Conventional wheat yields in the Midwest commonly range from 60 to 70 bushels per acre. Organic wheat yields typically range from 45 to 55 bushels per acre due to limited synthetic input usage and mechanical weed control practices.

Production costs also differ structurally. Conventional wheat depends heavily on synthetic fertilizers and herbicides, making it sensitive to global input markets. Organic wheat relies on crop rotation, soil health management, and labor-intensive operations.

Despite lower yields, higher market prices offset organic production constraints. This economic dynamic is central to long-term price trends for organic vs conventional wheat.

Profitability Modeling per Acre

Consider a simplified Midwest farm scenario.

A conventional wheat operation producing 65 bushels at $6.00 per bushel generates $390 in gross revenue per acre. After estimated costs of $280, net margin approximates $110 per acre.

An organic wheat operation producing 50 bushels at $12.00 per bushel generates $600 in gross revenue per acre. With estimated costs of $350, net margin approaches $250 per acre.

This margin differential illustrates why price trends for organic vs conventional wheat favor organic systems in long-term profitability modeling, provided demand remains stable.

Volatility and Risk Assessment

Conventional wheat prices exhibit higher volatility due to exposure to export restrictions, weather shocks, and speculative futures trading. Price movements of 20 to 40 percent within a single season are not uncommon.

Energy input costs often influence wheat production economics, and our deep dive into How Do Geopolitical Risks Impact Oil Supply Chains? explains how crude oil disruptions can indirectly affect fertilizer, freight, and grain pricing.

Conventional wheat volatility can be tracked directly through Chicago Board of Trade futures pricing available via CME Group’s official wheat contract page.

Organic wheat prices tend to move more gradually because they are anchored in contract-based supply chains. However, regional supply shortages or import fluctuations can still create pricing pressure.

Risk-adjusted return analysis suggests that price trends for organic vs conventional wheat reflect different volatility profiles rather than simple premium differences.

USDA-Style Forecast Model (2026–2035)

Under a base scenario, conventional wheat prices are expected to average between $6.00 and $7.50 per bushel through 2035. Organic wheat prices are projected to average between $11.00 and $14.50 per bushel. The structural premium remains near 70 percent.

In a bullish weather scenario, reduced supply could push organic premiums above 100 percent. In a bearish acreage expansion scenario, the premium may compress toward 50 percent but is unlikely to disappear entirely.

This forecast supports continued divergence in price trends for organic vs conventional wheat across long-term agricultural cycles.

For additional macro commodity forecasting insights, see our structured outlook in Bulk Aluminum Packaging Suppliers in Texas, where we model industrial pricing behavior under supply chain constraints.

Global production and trade projections from the Food and Agriculture Organization further support structural divergence in wheat markets

Demand Growth and Consumer Behavior

Organic wheat demand continues to grow at a faster pace than conventional wheat demand. Health awareness, institutional procurement, and premium retail positioning support sustained organic consumption growth.

Conventional wheat demand remains stable and is closely tied to export competitiveness and population growth. These contrasting demand dynamics reinforce persistent price trends for organic vs conventional wheat.

The Organic Trade Association’s annual industry survey documents continued expansion in certified organic grain demand, reinforcing long-term premium strength.

Strategic Implications for US Farmers and Investors

For farmers, organic wheat offers higher per-acre margin potential but requires disciplined management and certification compliance. Conventional wheat offers scale efficiency and access to hedging tools but carries greater macroeconomic exposure.

Investors comparing agricultural commodities may also benefit from our analysis on Regenerative Agriculture Impact on Soy Yields, which explores long-term yield stability and margin resilience in alternative crop systems.

For investors, conventional wheat provides liquid market access through futures contracts, while organic wheat reflects structural food inflation positioning. Understanding price trends for organic vs conventional wheat enables diversified agricultural strategy planning.

What This Means for U.S. Investors

For U.S. investors, price trends for organic vs conventional wheat present two distinct strategic exposures within the agricultural sector.

Conventional wheat offers liquidity and tradability through futures contracts and agricultural ETFs. Investors can hedge inflation, speculate on global supply disruptions, or gain short-term exposure to weather-driven volatility. Because conventional wheat prices are tightly linked to global exports and macroeconomic conditions, this segment behaves like a classic cyclical commodity.

Organic wheat, however, represents a structural premium segment within the food supply chain. While it is not directly traded on major futures exchanges, exposure can be obtained indirectly through organic-focused food producers, specialty grain processors, farmland REITs, or agricultural land investments transitioning into certified organic production.

From a portfolio perspective, conventional wheat provides tactical trading opportunities, while organic wheat aligns more closely with long-term structural themes such as:

- Food inflation resilience

- Consumer health trends

- Sustainable agriculture growth

- Margin durability in constrained supply systems

Investors evaluating price trends for organic vs conventional wheat should consider risk tolerance, liquidity needs, and investment horizon. Conventional wheat may suit shorter-term macro positioning, whereas organic exposure aligns better with long-duration agricultural value strategies.

Frequently Asked Questions

Why are price trends for organic vs conventional wheat structurally different?

Because organic production is constrained by certification timelines, while conventional wheat responds rapidly to global supply incentives.

Does organic wheat always trade at a premium?

Historically, organic wheat has maintained a consistent premium due to supply rigidity and demand growth.

Can the premium disappear completely?

A complete premium collapse is unlikely because acreage expansion is structurally limited.

Which market is more volatile?

Conventional wheat is generally more volatile due to futures market exposure.

Final Strategic Outlook

Price trends for organic vs conventional wheat demonstrate durable structural divergence rooted in supply elasticity, demand growth, and production economics. Organic wheat maintains premium resilience, while conventional wheat remains globally integrated and volatility-sensitive. Through 2035, sustained premium positioning appears more probable than convergence.

Disclaimer

This content is for informational purposes only. Agricultural markets are subject to weather variability, policy changes, regional cost differences, and global supply disruptions. Revenue examples are illustrative and may vary by operation.

Author

US Commodity Research Team

Independent agricultural market analysts specializing in structural price modeling, supply-demand forecasting, and long-term farm profitability research.