The tax implications of selling inherited gold coins can significantly affect how much money heirs ultimately keep after liquidation. While inheritance itself does not trigger income tax, selling inherited precious metals may create capital gains liability under IRS rules.

In the United States, inherited gold benefits from the step-up in basis rule. However, because gold coins are classified as collectibles, gains may be taxed at rates as high as 28%. Understanding the tax implications of selling inherited gold coins before making a transaction helps prevent unexpected liabilities.

The tax implications of selling inherited gold coins depend on the stepped-up cost basis at the date of death. When sold, gains are treated as long-term capital gains and may be taxed at the federal collectibles rate of up to 28%, plus any applicable state taxes.

Key Takeaways

- Inherited gold receives a stepped-up cost basis

- Sales qualify automatically as long-term capital gains

- Gold coins are taxed under the collectibles category

- Federal tax may reach 28%

- Accurate documentation reduces audit risk

Table of Contents

- Understanding the Tax Implications of Selling Inherited Gold Coins

- Step-Up in Basis Rule Explained

- Alternate Valuation Date Exception

- Capital Gains and Collectibles Tax Rate

- Estate Tax vs Capital Gains Tax

- Dealer Reporting and 1099-B Rules

- Federal and State Tax Calculation Example

- Tax Planning Strategies for Heirs

- What This Means for US Investors

- Frequently Asked Questions

- Final Thoughts

- Author

- Disclaimer

Understanding the Tax Implications of Selling Inherited Gold Coins

The IRS does not tax you at the moment you inherit gold coins. Taxation occurs only when you sell them.

The tax implications of selling inherited gold coins arise from capital gains. Capital gain equals the difference between the fair market value at inheritance and the final selling price. Inherited assets automatically receive long-term treatment, regardless of how long you personally hold them.

These rules form the foundation of how the tax implications of selling inherited gold coins are calculated under federal law.

The IRS provides detailed guidance on the sale of inherited assets in Publication 544.

Step-Up in Basis Rule Explained

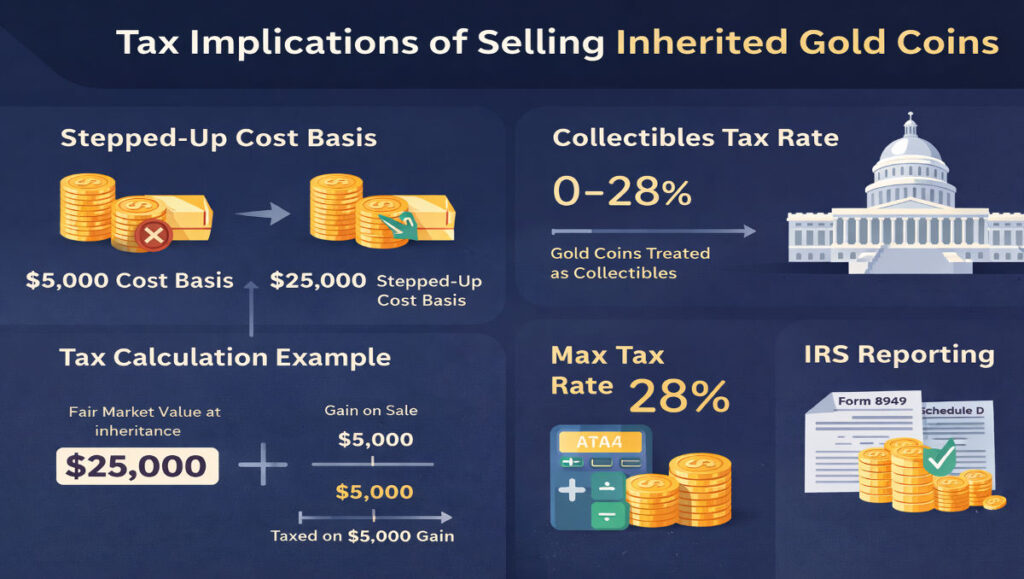

The step-up in basis rule resets the cost basis of inherited property to its fair market value on the date of the original owner’s death.

If gold coins were purchased decades ago for $6,000 but valued at $35,000 at inheritance, your basis becomes $35,000. If you later sell for $40,000, only the $5,000 gain is taxable.

This basis adjustment significantly reduces the tax implications of selling inherited gold coins compared to the original purchase price.

Alternate Valuation Date Exception

In certain estates, the executor may elect an alternate valuation date, which is six months after death. This option is used only if it reduces overall estate tax liability.

If chosen, the inherited gold coins receive a cost basis based on that alternate date rather than the date of death. This election can meaningfully change the tax implications of selling inherited gold coins, particularly during volatile gold markets.

Capital Gains and Collectibles Tax Rate

Gold coins are classified as collectibles under IRS rules. This classification changes how gains are taxed.

Unlike stocks, collectibles do not qualify for the standard long-term capital gains brackets of 0%, 15%, or 20%. Instead, gains may be taxed at a maximum federal rate of 28%.

These rules are central to understanding the tax implications of selling inherited gold coins in higher income brackets. If your ordinary income bracket is lower than 28%, your effective rate may also be lower.

Investors comparing gold taxation to other asset classes can also review our guide explaining what is the difference between spot price and futures price to better understand how precious metals pricing works before liquidation.

Official IRS capital gains guidance is available here.

Estate Tax vs Capital Gains Tax

Estate tax and capital gains tax are separate concepts.

Estate tax applies to the total value of a decedent’s estate before assets are distributed. Only estates exceeding the federal exemption threshold are subject to federal estate tax.

The tax implications of selling inherited gold coins relate primarily to capital gains, not estate tax. Most heirs do not personally pay federal estate tax.

Current federal estate tax rules can be reviewed on the IRS website.

Dealer Reporting and 1099-B Rules

Certain bullion transactions may trigger Form 1099-B reporting requirements. Reporting thresholds depend on the type and quantity of coins sold.

Even if a dealer does not issue a 1099-B, you remain responsible for accurately reporting gains. Maintaining estate valuation documents and appraisal records helps calculate the tax implications of selling inherited gold coins correctly.

Proper documentation is essential to avoid IRS scrutiny.

If you are evaluating the timing of a gold sale, monitoring real-time commodity markets can help. See our daily update on crude oil price today USA to understand broader commodity volatility trends.

Reporting requirements are explained in Schedule D instructions.

Federal and State Tax Calculation Example

Assume the fair market value at inheritance was $45,000. You later sell the gold coins for $55,000.

Your capital gain equals $10,000. If subject to the 28% collectibles rate, federal tax equals $2,800. If your state imposes a 5% capital gains tax, that adds $500.

Total tax equals $3,300, reducing net proceeds to $51,700. This example illustrates how the tax implications of selling inherited gold coins directly influence net outcomes.

Tax Planning Strategies for Heirs

Strategic timing can reduce tax exposure.

Selling during lower-income years may reduce your effective tax rate. Capital losses from other investments can offset collectible gains. Charitable donations of appreciated gold may eliminate capital gains entirely while providing a deduction.

Strategic planning can significantly reduce the tax implications of selling inherited gold coins when large gains are involved.

Those expanding their portfolio beyond bullion can review our strategy guide on how to invest in copper mining stocks for 2026 to understand tax exposure across commodity sectors.

What This Means for US Investors

For US investors managing inherited precious metals, evaluating the tax implications of selling inherited gold coins is essential before liquidation.

The step-up in basis rule offers meaningful protection against historic appreciation. However, post-inheritance price increases may still be taxed at the collectibles rate.

Before selling, heirs should verify valuation dates, confirm reporting obligations, and evaluate federal and state tax exposure. Fully assessing the tax implications of selling inherited gold coins helps preserve inherited wealth.

Investors diversifying beyond gold may also explore our analysis on where to buy palladium bars in California for insights into other precious metals markets.

Frequently Asked Questions

Do I pay tax when I inherit gold coins?

No. Tax applies only when you sell the coins.

Are inherited gold coins taxed as ordinary income?

No. They are taxed as long-term capital gains under the collectibles classification.

What is the maximum federal tax rate?

Up to 28% for collectibles.

Does holding the coins longer reduce taxes?

No. Inherited assets automatically qualify as long-term for tax purposes.

Final Thoughts

The tax implications of selling inherited gold coins depend on stepped-up basis rules, collectibles tax rates, valuation dates, and proper reporting.

While inheritance itself does not create immediate tax liability, selling inherited precious metals may trigger federal and state capital gains obligations. Before liquidating, heirs should carefully evaluate the tax implications of selling inherited gold coins to avoid unnecessary liabilities.

Author

US Commodity Price Research Desk

Independent analysts specializing in precious metals taxation, capital gains rules, and US investment compliance.

Disclaimer

This article is for informational purposes only and does not constitute tax, legal, or financial advice. Consult a qualified CPA or tax professional before making decisions regarding inherited assets.